"Suspending mark-to-market accounting, in essence, suspends reality."

Beth Brooke, global vice chair at Ernst & Young LLP, WSJ, Sept 30, 2008

"Blaming fair-value accounting for the credit crisis is a lot like going to a doctor for a diagnosis and then blaming him for telling you that you are sick."

analyst Dane Mott, JPMorgan Chase & Co., Bloomberg

"Suspending the mark-to-market prices is the most irresponsible thing to do. Accounting does not make corporate earnings or balance sheets more volatile. Accounting just increases the transparency of volatility in earnings."

Diane Garnick, Invesco Ltd., Bloomberg

Tuesday, September 30, 2008

Problem solved...it's always been that pesky "Mark to Market"

Forget rising consumer debt levels, home foreclosures, and the massive over supply of homes choking this market to death, Congress has found the root of the problem...Mark to Market.

Monday, September 29, 2008

Worst day since the 87 crash...

Interestingly, my tour through the "blogosphere" has revealed that despite the overwhelming bearish sentiment these past several days, weeks and even months (these are very smart people, not the "CNBC crowd") a lot of them weren't properly positioned to capitalize off this monumental meltdown.

Friday, September 26, 2008

Best post EVER about our two bailout options...

What the fuck is wrong with our ‘fearless leaders’? Don’t they know 75% of this country is littered with illiterate rubes who don’t know the difference between a bank and a banana? To the average main street, blue collar, idiot, it makes zero sense to give ‘their money’ to a banana. Hell, they would much rather prefer a nice big fucking stimulus check, so that they can go buy a new plasma.

So, on top of all the bullshit congress has put us through, over the last 10 years, now they feel it’s imperative to play a losers game of financial chicken with Wall Street, because the fucking factory workers in Pennsylvania think “those fat cats” from Wall Street “outta go to jail.”

Okay, how about this, Mr. Joey Bag o’ Donuts:

Your credit lines have been canceled. Your daughters student loan has been canceled. Your filthy factory, due to their lines of credit being turned off, has to fire you, in order to stay afloat. Now that you are unemployed, you need to tap your 401k plan to live, while you are in between jobs. Oh, sorry, the value of your retirement account is down 60%, because that “fucking bailout for those Wall Street honchos” failed. And, finally, your local grocery store just got shut down, due to lack of liquidity.

So, on top of all the bullshit congress has put us through, over the last 10 years, now they feel it’s imperative to play a losers game of financial chicken with Wall Street, because the fucking factory workers in Pennsylvania think “those fat cats” from Wall Street “outta go to jail.”

Okay, how about this, Mr. Joey Bag o’ Donuts:

Your credit lines have been canceled. Your daughters student loan has been canceled. Your filthy factory, due to their lines of credit being turned off, has to fire you, in order to stay afloat. Now that you are unemployed, you need to tap your 401k plan to live, while you are in between jobs. Oh, sorry, the value of your retirement account is down 60%, because that “fucking bailout for those Wall Street honchos” failed. And, finally, your local grocery store just got shut down, due to lack of liquidity.

Wednesday, September 24, 2008

Interesting thoughts from Marc Faber...

``I don't believe this is going to be solved in six months to a year,'' Faber said.

Faber also forecast the Standard & Poor's 500 Index will rally to as high as 1,350 points following the approval of the bailout plan because stocks are ``oversold.'' That level is about 14 percent higher than the gauge's close yesterday.

Still, ``I'm not playing that rally,'' he said. ``I'd rather think that stocks are not particularly cheap. We don't have a valuation bubble. We have an earnings bubble. In 2009, earnings will disappoint.''

Although I agree with Mr. Faber on all fronts, I still plan to time the market and play this impending "Bailout bounce" because frankly I am getting paid with my own money to do so ;-)

Faber also forecast the Standard & Poor's 500 Index will rally to as high as 1,350 points following the approval of the bailout plan because stocks are ``oversold.'' That level is about 14 percent higher than the gauge's close yesterday.

Still, ``I'm not playing that rally,'' he said. ``I'd rather think that stocks are not particularly cheap. We don't have a valuation bubble. We have an earnings bubble. In 2009, earnings will disappoint.''

Although I agree with Mr. Faber on all fronts, I still plan to time the market and play this impending "Bailout bounce" because frankly I am getting paid with my own money to do so ;-)

Tuesday, September 23, 2008

It is a Goldman world, we're just living in it...

True brilliance from Leonard

Some things you should know about Goldman

If you have five dollars and Goldman Sachs has five dollars, Goldman Sachs has more money than you.

There is no 'ctrl' button on a Goldman Sachs's computer. Goldman Sachs is always in control.

Goldman Sachs is suing Myspace for taking the name of what he calls everything around you.

Goldman Sachs destroyed the periodic table, because Goldman only recognizes the element of surprise.

Goldman Sachs can kill two stones with one bird.

Guns don't kill people. Goldman Sachs kills People.

There is no theory of evolution. Just a list of animals Goldman Sachs allows to live.

Goldman Sachs does not sleep. Goldman waits.

The chief export of Goldman Sachs is Pain.

Sorry but it looks like GS bonuses are still on!

Some things you should know about Goldman

If you have five dollars and Goldman Sachs has five dollars, Goldman Sachs has more money than you.

There is no 'ctrl' button on a Goldman Sachs's computer. Goldman Sachs is always in control.

Goldman Sachs is suing Myspace for taking the name of what he calls everything around you.

Goldman Sachs destroyed the periodic table, because Goldman only recognizes the element of surprise.

Goldman Sachs can kill two stones with one bird.

Guns don't kill people. Goldman Sachs kills People.

There is no theory of evolution. Just a list of animals Goldman Sachs allows to live.

Goldman Sachs does not sleep. Goldman waits.

The chief export of Goldman Sachs is Pain.

Sorry but it looks like GS bonuses are still on!

Real work sucks...

I was going through job training this past week. It's not a McDonalds-esque job but close enough. I will be working on campus (Cal Poly) making sure the gym and university plaza are running smoothly.

I also had to repair the entryway stairs to my condo because they were looking pretty dangerous. Apparently, watching a Business Major play the role of carpenter is one funny site, just ask my neighbors.

School just started on Monday, so for the next few days I'll be trying to adjust to my new routine (studying, blogging, job searching, exercising, etc.)

Friday, September 19, 2008

This is worse than socialism...

this is corporate welfare. We are robbing the taxpayers (teachers, doctors, nurses, fire fighters, coal miners, police officers, construction workers, retail workers, office workers, etc.) and using THEIR money to keep paying the salaries of greedy idiots and risky corporations. I am glad we avoided another Great Depression, because that's clearly where we were headed, but we can't just hit the "reset button" without causing someone pain.

THE RTC IS NOT DESIGNED TO MAKE TAXPAYERS MONEY!!! The government will buy these horrible loans (worth 22 cents on the dollar AT BEST) for 60-65 cents. After holding them for 5-7 years, the government will then sell the loans back to banks for 30 cents on the dollar (of course by then these loans will have appreciated considerably because the "bad" loans will have been purged during the 5-7 years of holding. DISGUSTING CORPORATE WELFARE!

P.S. My portfolio was up 8% today. I will give ALL the profits to charity.

THE RTC IS NOT DESIGNED TO MAKE TAXPAYERS MONEY!!! The government will buy these horrible loans (worth 22 cents on the dollar AT BEST) for 60-65 cents. After holding them for 5-7 years, the government will then sell the loans back to banks for 30 cents on the dollar (of course by then these loans will have appreciated considerably because the "bad" loans will have been purged during the 5-7 years of holding. DISGUSTING CORPORATE WELFARE!

P.S. My portfolio was up 8% today. I will give ALL the profits to charity.

Wednesday, September 17, 2008

Our government's message to the financials...

Hat tip to I-bank Coin ("The Fly" is truly a mad genius)

Wonder why Goldman and Morgan Stanley were down even after AIG's bailout?

Given AIG's exposure to the credit default swap (CDS) market, I thought that their bailout would be cheered, instead the financials were DESTROYED today. Here's why:

THIS IS MARKET MANIPULATION IN ITS PUREST FORM! These funds will do anything for alpha. Granted I think financial stocks aren't worth a warm bucket of p*ss at this stage in our economic collapse, but they shouldn't be "euthanized" by these hedge funds like this.

I use the ugly term "euthanize" because this current process of eliminating weak financials (Fannie, Freddy, and now AIG) is completely unnatural in a properly functioning "market" (I use that term loosely given all these bailouts). I am all for shaking out the bad companies in an economy, but not in such a chaotic manner.

By continuously "bear raiding" banks' common stock, hedge funds are inducing a hastened ratings downgrade and a consequent short term liqidity crunch (AIG had to cough up $40 billion practically overnight because of a downgrade caused by these disorderly bear raids). These funds are not letting the market slowly destroy these stocks, rather they are exploiting relaxed short selling rules to hasten the "departure" of many weak players. In other words, manipulating stocks as they (not the market) see fit.

THIS IS MARKET MANIPULATION IN ITS PUREST FORM! These funds will do anything for alpha. Granted I think financial stocks aren't worth a warm bucket of p*ss at this stage in our economic collapse, but they shouldn't be "euthanized" by these hedge funds like this.

I use the ugly term "euthanize" because this current process of eliminating weak financials (Fannie, Freddy, and now AIG) is completely unnatural in a properly functioning "market" (I use that term loosely given all these bailouts). I am all for shaking out the bad companies in an economy, but not in such a chaotic manner.

By continuously "bear raiding" banks' common stock, hedge funds are inducing a hastened ratings downgrade and a consequent short term liqidity crunch (AIG had to cough up $40 billion practically overnight because of a downgrade caused by these disorderly bear raids). These funds are not letting the market slowly destroy these stocks, rather they are exploiting relaxed short selling rules to hasten the "departure" of many weak players. In other words, manipulating stocks as they (not the market) see fit.

Tuesday, September 16, 2008

AIG is the epitome of "Too big to fail"

That's why it will be bailed out. I have no doubt in my mind. However, as their "punishment," AIG equity holders should be crushed like GSE stockholders (see Bill Miller). Looking at the overall catastroph*ck going on, I am reminded of these wise words:

“If they are too big to fail, make them smaller.”

-Former Treasury Secretary George Shultz

P.S. Given AIG's global embarrassment, they should never be allowed to advertise on sports teams again.

“If they are too big to fail, make them smaller.”

-Former Treasury Secretary George Shultz

P.S. Given AIG's global embarrassment, they should never be allowed to advertise on sports teams again.

Monday, September 15, 2008

Cool graph on Commercial Real Estate...

On second thought this might not be such a "cool" graph. I mean aren't we already f*cked in this economy. Oh well, my philosophy is: "Better to grasp the Universe as it really is, than to persist in delusion."

Talk about a shotgun marriage..Merrill Lynch and Bank of America

I am still scratching my head and wondering: If Merrill Lynch sold itself for a 70% premium, then why did it need to sell itself at all?

I think we all know the answer to that one. Thain took a look at Merrill's book and knew that it couldn't survive any further write downs without completely diluting (aka wiping out) the equity holders and sovereign funds. I mean they had already diluted them out to the tune of 30%.

Anyway, I was stunned to hear how quickly this deal was finalized. It happened so fast that even Thain doesn't know what his official role will be yet.

The question now becomes: Did Lewis even really inspect Merrill's books before diving in? Given Lewis's rash decision to buy Countrywide, I wouldn't be surprised if Lewis said yes in two seconds.

I think we all know the answer to that one. Thain took a look at Merrill's book and knew that it couldn't survive any further write downs without completely diluting (aka wiping out) the equity holders and sovereign funds. I mean they had already diluted them out to the tune of 30%.

Anyway, I was stunned to hear how quickly this deal was finalized. It happened so fast that even Thain doesn't know what his official role will be yet.

Thain said he contacted Bank of America Chairman and Chief Executive Ken Lewis Saturday morning and proposed a merger as concerns swirled over whether Merrill could meet the same fate as Lehman. Thain said the deal made strategic sense, and Lewis said he was interested immediately, adding that Merrill could have easily gone elsewhere for a merger partner.

"Better to seize on this opportunity as we see it in the moment," Lewis said. He added later: "It didn't take but about two seconds to see the strategic implications, the positive implications."

The question now becomes: Did Lewis even really inspect Merrill's books before diving in? Given Lewis's rash decision to buy Countrywide, I wouldn't be surprised if Lewis said yes in two seconds.

Are you kidding me? Wells Fargo was actually up today!

Efficient market my ass. WFC is NOT one of the best. If anything it's one of the best con men around. Did I say con men? I meant banks. In fact, Mr. Mortgage de-bunked WFC's "beat" last July very effectively:

Also WFC has $84 Billion in their Home Equity Line/Loan portfolio (1/2 located in hard hit states like CA & FL). Given the massive house price depreciation we have seen, I seriously doubt that their Q2 loan loss provision of $3 billion will be sufficient (Hell just today UBS announced another $5 billion in write offs).

If all that weren't bad enough, WFC just said it would take a charge on $480 million worth of exposure to Fannie and Freddie preferred shares.

Conclusion: Wells Fargo is in trouble

“In the second quarter, Wells Fargo changed its policy toward charged-off home equity loans to 180 days delinquent from 120 days “to provide more time to work with customers to solve their credit problems and keep them in their homes,” the company said on Wednesday. The change deferred roughly $265 million of charge-offs in the second quarter. Approximately 900 customers with $90 million of home equity loans have been modified due to the change, Wells Fargo said.”

Also WFC has $84 Billion in their Home Equity Line/Loan portfolio (1/2 located in hard hit states like CA & FL). Given the massive house price depreciation we have seen, I seriously doubt that their Q2 loan loss provision of $3 billion will be sufficient (Hell just today UBS announced another $5 billion in write offs).

“As second lien borrowers see equity in their homes evaporate due to price depreciation, second liens become extremely vulnerable to loss. Which is why this stat matters more than most: approximately $35.6 billion of Wells Fargo’s $84 billion in home equity loans had combined loan-to-value ratios above 90 percent, according to the second quarter report. And that’s a figure based on automated value models, or AVMs, that were run in March 2008; were those AVMs run again today, it’s almost a sure bet that the number has gone up even further.”

If all that weren't bad enough, WFC just said it would take a charge on $480 million worth of exposure to Fannie and Freddie preferred shares.

Conclusion: Wells Fargo is in trouble

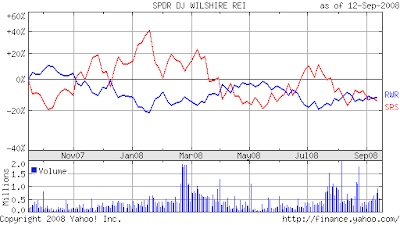

First major epiphany: Commercial REITS are still overpriced

Here's a chart of the RWR (Dow Jones Wilshire REIT index):

As you can see it is down this past year, but given the macro fallout from de-levering banks (i.e. slower economic growth, higher unemployment, tougher credit standards) I believe commercial real estate will suffer considerably. I'll have stats and numbers justifying this call shortly. In the meantime I'll leave you will some quotes about the status of commercial REITS going forward (this was after CB Richard Ellis missed earnings on July 30th):

IMO, the best way to play the impending price correction in commercial real estate is through the SRS:

As you can see it is down this past year, but given the macro fallout from de-levering banks (i.e. slower economic growth, higher unemployment, tougher credit standards) I believe commercial real estate will suffer considerably. I'll have stats and numbers justifying this call shortly. In the meantime I'll leave you will some quotes about the status of commercial REITS going forward (this was after CB Richard Ellis missed earnings on July 30th):

Goldman Sachs analysts following the company said that CB Richard Ellis was hit by "sharply weaker commission-based investment sales and leasing revenues, both in the U.S. and globally ... which reaffirms our view that a recovery in the back half of 2008 seems unlikely

"The unwinding of the U.S. housing- and mortgage-market euphoria has produced tremors that at midyear 2008 have reached seismic proportions," said Ray Torto, global chief economist at CB Richard Ellis.

Lack of liquidity in capital markets and deteriorating fundamentals are having a negative impact on real-estate investment trusts and related companies, according to Goldman analysts.

"The decline and variance to our estimate was due primarily to a material drop-off in both the property-sales and leasing businesses, and was evident across all regions," wrote Ross Smotrich at Lehman Brothers in a report on CB Richard Ellis. "To the extent that CB Richard Ellis' business is a leading indicator for real-estate fundamentals, the quarter may not bode well for the second half of the year."

IMO, the best way to play the impending price correction in commercial real estate is through the SRS:

Sunday, September 14, 2008

Lehman's officially a goner...

Truly amazing...

Unfortunately we are only in the beginning (top of second inning) for what will be the de-levering of the American financial system. I just pray "main street" won't catch up to where Wall Street finds itself because if that happens, we will be looking at 10%+ unemployment with high inflation. That combination will result in massive negative feedback loops (think home foreclosures, auto and credit card defaults) for millions of families. Mind you these aren't "subprime" families, they are just "collateral" damage.

Worse yet, if this implosion occurs (once again I hope it doesn't) it will likely stunt the "Global growth" story for millions of people looking to raise themselves out of poverty (the only bright spot in this messed up world).

Unfortunately we are only in the beginning (top of second inning) for what will be the de-levering of the American financial system. I just pray "main street" won't catch up to where Wall Street finds itself because if that happens, we will be looking at 10%+ unemployment with high inflation. That combination will result in massive negative feedback loops (think home foreclosures, auto and credit card defaults) for millions of families. Mind you these aren't "subprime" families, they are just "collateral" damage.

Worse yet, if this implosion occurs (once again I hope it doesn't) it will likely stunt the "Global growth" story for millions of people looking to raise themselves out of poverty (the only bright spot in this messed up world).

Nothing ever goes to plan....

I am livid:

I got called into work on Saturday, so obviously my research trip to the blogosphere was short lived. I'll try to get this sh*t done before Wednesday.

I got called into work on Saturday, so obviously my research trip to the blogosphere was short lived. I'll try to get this sh*t done before Wednesday.

Friday, September 12, 2008

I am popping pills this weekend...

I took Thursday and Friday off from my work on campus to relax. I will be spending the remainder of my weekend in "Wonderland" (aka the blogosphere) combing over reports by people more intelligent than myself to figure out what the future holds for this market of stocks. In case you are wondering I have no friends and my parents have vowed never to speak with me ;-) I fully expect that I will return from "vision quest" knowing just how deep the rabbit hole goes. Drop by Monday and I will share my wisdom with you.

Wednesday, September 10, 2008

Most important graph you'll ever see...

The implications of this graph, compiled by Credit Suisse, are profound in terms of future write-offs, credit availability, bank solvency, economic growth and unemployment (both in the U.S. and globally). If you think it's bad now, you ain't seen nothing yet.

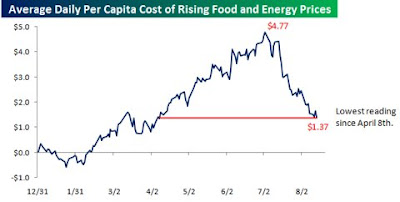

Falling commodities are the only saving grace...

I am convinced the only thing that is preventing this market from really plummeting is the removal of the commodity headwind (ie rising energy and food prices). The rationale being that consumers will have more disposable income as costs subside. Of course, this "removal" is merely an illusion as this graph points out:

Conclusion: "Removing" this commodity headwind saves consumers a whopping $24 dollars a week ($3.4 x 7). I guess we better go buy retail stocks and domestic equities ;-)

Conclusion: "Removing" this commodity headwind saves consumers a whopping $24 dollars a week ($3.4 x 7). I guess we better go buy retail stocks and domestic equities ;-)

There is no safe harbor...

*I find it very ironic that the weakest sectors (consumers and credit related) are holding up the best, of course consider how much taxpayer money has been thrown their way.

Monday, September 8, 2008

Another post about solar...

Looking at these stats, I think Sunpower and Wall Street are being way too optimistic that the average selling price of a photovoltaic modules (the ASP of a PV mod) won't fall 20% plus (Wall Street overconfident? Never :-)

Apparently this new supply figure was upwardly revised:

A big reason I like this study is because they went through more than 100 solar companies and approached the problem from bottom-up approach:

The sheer lack of barriers to entry right now in solar is astonishing:

Thin-film solar production is expected to double in each of the next three years to reach 4.18 gigawatts worth of equipment in 2010, according to a report to be released by Greentech Media and the Prometheus Institute on Tuesday.

Apparently this new supply figure was upwardly revised:

The forecast represents a 65 percent increase from the companies' previous projection 18 months ago, according to the report. The authors also forecast that production will continue to grow, reaching almost 10 gigawatts in 2012.

A big reason I like this study is because they went through more than 100 solar companies and approached the problem from bottom-up approach:

The projections are based on a survey of 137 companies. According to the report, at least 143 companies were participating in thin-film solar as of July, with nearly 40 companies entering the space in 2007 and an additional 23 companies joining the movement in the beginning of this year. This implies that nonparticipating companies, as well as new companies yet to enter the field, could end up pushing the numbers even higher.

The sheer lack of barriers to entry right now in solar is astonishing:

All together, Grama and Bradford expect only eight of 144 firms to reach "significant production" – defined as more than 25 megawatts of production – this year, increasing to around 30 companies by 2010.

I prefer the long run...say 6-9 months

I am not a day trader, but this market is so volatile that I find myself hitting my price targets or stop losses (lately it's been the latter) VERY quickly. Furthermore, given how precarious the global financial markets (ie hedge fund's blowing up) I don't want to overstay my welcome in certain stocks (even if the stocks that I like have 3-5 years of auspicious earnings visibility ahead of them).

With that said there are some "trends" that even this impatient & bi-polar market acknowledges and one of them is the impending solar surplus that should hit in 2009.

Bear case number one for the solar surplus is pretty mild:

However, some of the biggest solar companies aren't sounding as sunny (couldn't help myself) in their assesments, which brings us to bear case number two:

The biggest x-factor in all this is whether the U.S. (currently 10% of global demand - a pathetic number indeed) and other governments step up to absorb the surplus and invest in their future energy infrastructure.

With that said there are some "trends" that even this impatient & bi-polar market acknowledges and one of them is the impending solar surplus that should hit in 2009.

Solar stocks were pummeled on Monday as investors fretted that an oversupply of solar panels next year will drive down prices and profit margins in the high-flying sector.

Bear case number one for the solar surplus is pretty mild:

Solar companies, Hoopes and other analysts said, have said price declines will be in the 5 to 10 percent range next year and that demand will remain healthy despite a pullback in government solar subsidies in Spain, one of the biggest solar markets.

However, some of the biggest solar companies aren't sounding as sunny (couldn't help myself) in their assesments, which brings us to bear case number two:

U.S. solar company SunPower told Reuters at an industry conference last week that it could see a price decline of 10 to 20 percent next year -- adding fuel to the share declines of the last few days

The biggest x-factor in all this is whether the U.S. (currently 10% of global demand - a pathetic number indeed) and other governments step up to absorb the surplus and invest in their future energy infrastructure.

"We still don't believe the bull thesis," Oppenheimer analyst Sam Dubinsky wrote in a client note on Monday, adding that it was too soon to tell whether markets including the United States, France, Italy and Greece would absorb the solar panels that won't be sold to Spain.

Trade of the week...

We are still in a bear market, I don't care if the Feds are "injecting" Fannie and Freddie with money. However, the market has been oversold and this news might be enough the reassure some institutions to nibble (almost all of the "big swinging d*cks" have considerable cash positions that they need to put to use eventually). I am going to play this "moral hazard" game with the market by taking considerable long positions in GFA (a homebuilder albeit Brazilian), GSI (which seems to have held support), and MOS (this one has the tightest stop at 90)

LONG:

GFA (tp 30.5, stop 26)

GSI (tp 13, stop 10.50)

MOS (tp 98, stop 90)

UPDATE

I hit my stop loss with MOS corp. (These hedge fund liquidations are the equivalent of land mines when it comes to investing - all seems fine and then BOOM)

LONG:

GFA (tp 30.5, stop 26)

GSI (tp 13, stop 10.50)

MOS (tp 98, stop 90)

UPDATE

I hit my stop loss with MOS corp. (These hedge fund liquidations are the equivalent of land mines when it comes to investing - all seems fine and then BOOM)

Friday, September 5, 2008

Still a bear market but...

nothing goes down in a straight line (we will have our fair share of dead cat bounces). I added to my Molybdenum position today by buying some more of Thompson Creek (TC) - but it was just a nibble. I'll do a report later today on Moly's fundies to justify my selection of this egregiously poor performing stock.

Thursday, September 4, 2008

We will retest the July lows...

So the options are:

a) Short this market

b) Continue to keep your powder dry and wait for the bounce (I am 50% cash)

Whichever you choose, DO NOT buy yet. Wait for how this market reacts at the July lows (ie see if there are any buyers). Very few investors can perfectly time a bottom (so I'll gladly take 70% of a stock move and miss the first 30% then buy into a bull trap). Remember, capital preservation is far more important than capital growth. Your first job isn't to make money, it's to NOT LOSE money. Think in terms of baseball and "wait for your pitch." I am done with the cliches.

Wednesday, September 3, 2008

Gafisa is finally dealing...

I've been waiting for Gafisa, one of Brazil's most promising stocks, to use its excess cash (it's really Sam Zell's cash :-) to make some acquisitions. Well recently Gafisa made a move that will increase its exposure to Brazil's booming housing market (Brazil has a glut of around 7 million homes).

According to analysts, both Gafisa and Tenda will enjoy synergies in the low-income market; I also see that UBS upgraded GFA upon hearing this news. I am also happy with Gafisa's surprise timing with this deal(even the experts weren't expecting M&A until 2009 or 2010).

I started a position in GFA today as it has pulled backed significantly since the Tenda deal. Nevertheless the chart is awful and I expect more pain ahead (hence the dollar cost averaging).

As an aside, it obvious that most of the BRIC/Commodity plays are getting slaughtered. Whether or not it's due to hedge fund redemptions or the impending global depression, all I can say is that you shouldn't invest in these names unless you have a 5-10 year time horizon, otherwise you will get scared out of them fast.

Position: Long Gafisa

Gafisa SA, Brazil's second-largest real estate developer, agreed to buy a controlling stake in rival Construtora Tenda SA, aiming to boost its presence in the low- income housing market. The companies' shares surged.

As part of the transaction, Gafisa will have a 60 percent stake in Tenda, while Fit Residencial Empreendimentos Imobiliarios Ltda., the Gafisa subsidiary focused on low-income housing, will be part of Tenda, Sao Paulo-based Gafisa said in a statement on the Brazilian securities regulator's Web site.

According to analysts, both Gafisa and Tenda will enjoy synergies in the low-income market; I also see that UBS upgraded GFA upon hearing this news. I am also happy with Gafisa's surprise timing with this deal(even the experts weren't expecting M&A until 2009 or 2010).

I started a position in GFA today as it has pulled backed significantly since the Tenda deal. Nevertheless the chart is awful and I expect more pain ahead (hence the dollar cost averaging).

As an aside, it obvious that most of the BRIC/Commodity plays are getting slaughtered. Whether or not it's due to hedge fund redemptions or the impending global depression, all I can say is that you shouldn't invest in these names unless you have a 5-10 year time horizon, otherwise you will get scared out of them fast.

Position: Long Gafisa

Tuesday, September 2, 2008

An appropriate metaphor?

I am thrilled to hear the levees held up. The people in New Orleans & Louisiana have had enough bulls**t to deal with in their lives.

However, looking at this photo I am reminded about how dangerously vulnerable our country is right now. Obviously our country is fighting two wars, and our physical infrastructure is shot to hell, but what about our financial infrastructure?

Personally, I do think our financial system is strong enough to weather this storm in the long run, but in the short term (1-5 years) its obvious that our "financial levees" will ultimately give way. When will the "break" occur? I don't know. What I do know is that there are still 100's of billions of securitized credit card loans, car loans, alt-a POA's, heloc's and commercial real estate loans that will go bad.

Ultimately, it will take many more years before we de-leverage our banks and our consumers (ie our negative savings rate) to responsible levels. The housing boom was just a manifestation of this country's love affair with debt and over consumption (America had a very similar "fling" during the roaring 20's, which didn't end well). Of course, beyond changing our individual lifestyles, this country must also address its current accounts (think exports vs imports) and budget deficits so that we can avoid a hard-landing in the form of foreigners cutting off our lines of credit.

Fortunately for NOLA residents, their levees were able to weather a CAT 2 Hurricane like Gustav, I wish I could say the same for our financial levees, which appear overwhelmed in the face of a CAT 5 credit crisis.

{kind=link}

However, looking at this photo I am reminded about how dangerously vulnerable our country is right now. Obviously our country is fighting two wars, and our physical infrastructure is shot to hell, but what about our financial infrastructure?

Personally, I do think our financial system is strong enough to weather this storm in the long run, but in the short term (1-5 years) its obvious that our "financial levees" will ultimately give way. When will the "break" occur? I don't know. What I do know is that there are still 100's of billions of securitized credit card loans, car loans, alt-a POA's, heloc's and commercial real estate loans that will go bad.

Ultimately, it will take many more years before we de-leverage our banks and our consumers (ie our negative savings rate) to responsible levels. The housing boom was just a manifestation of this country's love affair with debt and over consumption (America had a very similar "fling" during the roaring 20's, which didn't end well). Of course, beyond changing our individual lifestyles, this country must also address its current accounts (think exports vs imports) and budget deficits so that we can avoid a hard-landing in the form of foreigners cutting off our lines of credit.

Fortunately for NOLA residents, their levees were able to weather a CAT 2 Hurricane like Gustav, I wish I could say the same for our financial levees, which appear overwhelmed in the face of a CAT 5 credit crisis.

Subscribe to:

Posts (Atom)